A Brexit mixed bag for meat

13th January 2017 by Cedric Porter

In the third of our special series, supply chain expert and former Oxford Farming Conference chairman Cedric Porter discusses the impact of Brexit on the meat sector.

Brexit is potentially a real Curate’s egg for the British meat industry. The UK’s reliance on imported meat, much of it from the EU, means that there is plenty of potential to produce more meat for British consumers, while longer-term opportunities lie outside the UK. But meat producers could be the most vulnerable from changes in support and the sheep industry’s reliance on imports means that it could suffer from a poor post-Brexit trade deal.

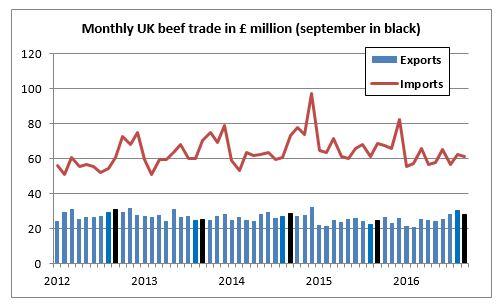

AHDB figures show that in 2015 the UK only produced the equivalent of 75% of the beef, 92% of the sheepmeat, 55% of the pigmeat and 73% of the poultry it consumed in 2015. Trade has always been important to the UK meat industry with 16% of UK beef exported, 27% of sheepmeat, 26% of pigmeat and 19% of poultry.

The EU is absolutely vital as both a supplier and customer of meat and the UK’s trading relationship with the 27 country union will be key to the future of the UK meat industry. Exports to the EU by value account for 65% of total exports for pigmeat, 70% for poultry and more than 90% for beef and sheepmeat. The EU supplies the UK with more than 90% of its beef, pigmeat and poultry needs, but less than 20% of its sheepmeat import needs because of the reliance on trade from New Zealand.

The weakening of the pound has given the UK meat industry a short-term boost with cattle prices 2% higher than a year ago, sheep prices 5% higher and pigmeat prices 14% higher.

It is the sheepmeat industry that is perhaps the most vulnerable to Brexit. Because the vast majority of sheepmeat exported from the UK is destined for the EU, virtually all shipments attract no import duties and tariffs. There is no guarantee that arrangement will continue after Brexit. Any duties or restrictions, even low or lenient ones, may push up export prices and damage EU demand. If no deal is done then trade relationships would revert to World Trade Organisation rules, which the AHDB estimates would have increased 2015 sheepmeat export prices by as much as 50%. That would be likely to have a devastating effect on the industry.

WTO restrictions would add up to 80% to the price of beef, according to the AHDB as well as 50% to pig carcasses and as much as 90% to the price of processed chicken. The high levels of these tariffs are likely to spur both the UK and EU to do a trade deal that sees much lower levels of duties and restrictions because it is in the interest of both parties, with the EU losing out significantly from any UK import restrictions because of the volume of meat trade it does with Britain. Ireland is at the forefront of efforts to ensure that a free meat trade deal will be done between the UK and EU because of the value of its beef trade with Britain.

As with all other products, it is important the UK meat industry does not take its eye off the ball and lose out on export opportunities outside the EU. My analysis suggests that world meat production will need to increase by 90% by 2050 if it is to keep up with world demand. With European population growth effectively static and meat consumption per head falling across the continent, all the growth in the world market is going to take place outside Europe with demand in Africa and Asia particularly strong.

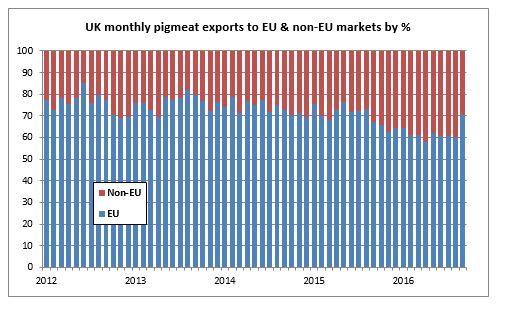

One UK sector that has particular success in diversifying into non-EU markets is pigs. Deals with China have allowed it to sell pork there and that has meant that in some months 40% of UK pigmeat exports by value are outside the EU.

Support inspiration

The pig and poultry industry may also give some inspiration to the other meat sectors on trading without agricultural supports. Historically only beef and lamb were specifically supported through the Common Agricultural policy. More recently, support was extended to all farms, although that made little difference on many intensive pig and poultry farms.

The pig and poultry industries have contracted much faster than pig and sheep sectors. In the 20 years to 2014 the number of breeding sow farms fell by 38% to just 6,000, while a tiny minority of the 2,500 poultry farms in the country produce the majority of birds. In contrast, the number of UK beef herds remains relatively stable at around 26,000 with 68,000 sheep flocks. The extensive nature of much of the UK’s beef and sheep production means that it is unlikely that contraction in those sectors will be so dramatic as in pigs and poultry, but if agricultural supports are withdrawn then it is inevitable that the number of red meat farms will decrease.

- UK beef production has fallen by 16% since 1991

- UK sheep production has fallen by 23% since 1991

- UK pigmeat production has also fallen by 23% since 1998

- UK meat consumption per head is falling with only poultry showing growth

- World meat demand is set to double by 2050