Dairy looks for post-Brexit boost

1st December 2016 by Cedric Porter

In the third of our special series, supply chain expert and former Oxford Farming Conference chairman Cedric Porter discusses the impact of Brexit on dairying.

The Brits like their milk with average dairy consumption at more than 115 kg/head/year. That is a little ahead of the Americans, and a little behind Dutch dairy devotees.

But despite its long history of dairy production and its natural climatic advantages, the UK does not produce enough milk to meets its own needs by a big margin. Production and consumption of liquid milk along with milk powder and cream may be in balance but Defra figures show that the UK only produces 75% of the butter it needs, just over half the cheese and 70% of the yoghurt it needs. The fact that the UK is not self-sufficient in dairy is largely due to the European Union which imposed quotas on production back in 1984 that meant the UK was not allowed to produce more than about 80% of the milk it needed to supply its own population. Those restrictions have now been removed, but many will argue they have done long-term damage to the UK dairy industry.

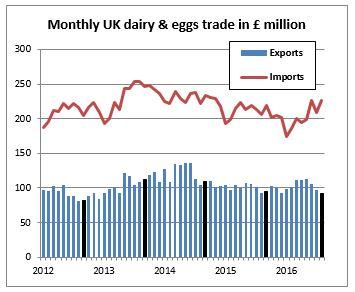

When it comes to trade in dairy, the UK also seriously lags behind. In August HMRC figures show that £227 million of dairy and egg imports came into the UK while £91 million were exported, a deficit of £136 million.

The UK dairy industry will be hoping that the decision to leave the EU will give it a unique opportunity to re-align itself and produce more milk and reduce imports. There are some reasons for optimism.

In the short term the weakening of the pound has made imports more expensive and given a boost to home produced products that are also more competitive when exported. In the longer term, the performance of the UK dairy industry will be influenced by the terms of any post-Brexit trade agreements. Currently, along with all other products, there are no tariffs or duties on dairy trade between the UK and all other parts of the EU. If no trade deal is done then trade may have to be done under World Trade Organisation rules. That could lead to tariffs (on both exports and imports) of between €7.0/100kg for whey to €221.2/100kg for some cheeses.

The AHDB calculates that at 2015 prices that could add up to 74% to the price of some dairy products. If that scenario were to play out it would dramatically affect the dairy market. Because of the large UK dairy trade deficit, the greatest impact would be on imports raising their price. That could reduce imports to the benefit of the UK industry. However, much higher import prices could be politically unacceptable for the UK Government and economically unacceptable for the EU, so it is likely that there will either be no tariffs or much lower tariffs than the WTO ones. But unless there is a single market as there is now, then trading between the EU and the UK is going to be somewhat more difficult than it is now either in terms of the imposition of small tariffs or extra paperwork which will add to costs and possibly reduce both imports and exports.

The UK has some natural dairy advantages whether it is in the EU or not. There are probably only a half dozen countries in the world that can grow as good a grass crop as the UK, while the country has a large and growing population that likes dairy products. The UK is also a world-class performer when it comes to dairy yields which are around 8,000 litres a cow a year, putting it in the top ten yielding countries in the world. Costs of production are also lower on many UK dairy farms than Continental ones, especially those can maximise the value of home-grown forage.

| Country | Yield |

|---|---|

| USA | 9,901* |

| Sweden | 8,518 |

| Estonia | 8,418 |

| Finland | 8,362 |

| Saudi Arabia | 8,340* |

| UK | 8,009 |

| Czech Republic | 7,877 |

| New Zealand | 4,379* |

Source: Eurostat & FAOSTAT (*l/year). EU figures 2014, others 2013

Although the UK dairy industry has a number of advantages that could mean it thrives in a post-Brexit market, it will have to ride the price volatility of the market, reduce imports and invest in production and processing if it is to do so. The prize is there, but it will take vision and dedication if it is to be won.

• The number of UK dairy producers has dropped by nearly a third in the last 20 years to just 13,000¹

• The number of dairy cows has fallen by a quarter in the last 20 years to 1.895 million¹

• EU dairy production has risen by 12% since 2010¹

• Global dairy demand is likely to increase by 56% by 2050 to 1.304 billion tonnes²

• In the 50 years to 2010 Chinese dairy consumption rose by 1,450% to 28.4 kg/head/year³

Sources:

¹ AHDB Dairy

² Supply Intelligence calculations

³ UN FAOSTAT