To Brexit and Beyond - trading & support

7th October 2016 by Cedric Porter

In the first of a special series, supply chain expert and former Oxford Farming Conference chairman Cedric Porter discusses farming’s hottest topic.

The Oxford Farming Conference has a reputation for helping to set the farming agenda for the year ahead. That has never been more so than in 2016 when a spirited debate between EU farm commissioner Phil Hogan and former Environment Secretary Owen Paterson set out the pros and cons of the UK’s membership of the European Union. Within weeks of the conference a referendum had been announced and by the middle of the year the theoretical had become the actual and Britain had voted to leave the EU.

The majority of farmers are thought to have voted out with a Farmers Weekly poll in April putting the Brexit vote at 58%. That surprised many because of the direct support that farmers receive from the EU’s Common Agricultural Policy. The UK receives around €3 billion a year in direct support to farmers and a further €1 billion in rural development funding. Most of this funding is from the EU and that will continue as long as the UK is still in the EU. Chancellor Philip Hammond has also committed to continue direct payments until 2020, which may mean that the Treasury will need to find at least one year’s funding.

But what will happen after 2020 is still anyone’s guess. Plenty of ideas are swirling around including the UK funding the status quo, a switch to just environmental payments, enhanced payments up to 50 hectares and then a tailing off of support after that and the capping of payments. Whatever the option, it will have to be funded by the UK taxpayer meaning that farmers will have to compete for funding with other sectors such as the health service, education and defence. There may be public support for maintaining landscapes and keeping family farms viable, but it is unlikely that large scale direct payments will gain much support.

Trading places

There are also those both in and out of the farming industry who see the Brexit vote as a unique opportunity to abandon direct support and give farmers the freedom to farm. Perhaps the most celebrated exponent of the non-subsidy route is New Zealand. It abandoned direct support in the mid-1980s and there is evidence it transformed its farming industry. Within 30 years wheat yields had risen by 125% and the country had become a global dairy superpower. Abandoning most support would be painful, but it could result in an agricultural industry that is more geared up to feeding the mid-21st Century world.

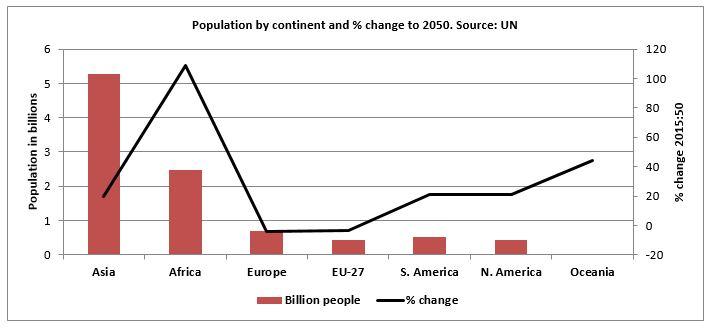

In or out of the EU, Europe’s power is declining. With the UK 6.7% of the world’s population lives in the EU, without the UK it is just 6.2%. Without the UK or any new entrants the EU is expected to be just 4.2% of the 9.725 billion world population by 2050. If the European farming industry is to thrive it will have to look beyond the continent for growth. The population of a UK-less EU is set to fall by 3.5% by 2050. Contrast that with the African population that is set to double by 2050. Ironically, one of the key issues of the referendum – the UK population – does provide opportunities for British farmers and others. It is set to grow by 15% by 2050, a stark contrast to countries such as Germany, Poland and Spain where population are falling.

The UK is already making some progress is selling more outside the EU, but its growing and gastronomically adventurous population mean it is still a target for imports. Food and Drink Federation figures for 2015 show that the UK imported £22.8 billion more food and non-alcoholic drinks than it exported. The EU accounted for 72.2% of exports, but the fastest growing markets were mainly outside the EU including a doubling of trade with Thailand and a 9.0% increase in exports to China. But Ireland remains the UK’s single biggest market at £2.9 billion, more than twice the size of second placed France. The strong pound impacted on British sales in 2015, so a short-term positive impact of Brexit could be that a weaker pound drives exports this year.

The future of agricultural support may be one of the main concerns among many farmers, but countering imports and building exports will be just as important for its long-term prosperity. That poses challenges for the Government as it negotiates trade deals, but also for farmers and the food industry in making sure they are producing the products the world wants.

In the run up to the 2017 Oxford Farming Conference Cedric Porter will look at how Brexit may impact on each farming sector.

Brexit facts

• The CAP costs the EU€57 billion a year, around €0.30 a day per EU citizen¹

• France receives 23% of direct CAP payments, the UK 9%¹

• The EU population is growing at 0.2% a year, the UK’s at 0.6% a year and Ireland’s at 1.2% a year²

• By 2050 the EU population is expected to be 408 million, only 10 million more than Nigeria and less than a quarter of India³

• In 2015 food and non-alcohol exports to the EU were £8.9 billion and £3.4 billion outside the EU⁴

• The pound is 24% weaker against the US$ than it was two years ago⁵

Sources:

¹ EU, ² CIA World Factbook, ³ UN, ⁴ Food & Drink Federation, ⁵ Bank of England